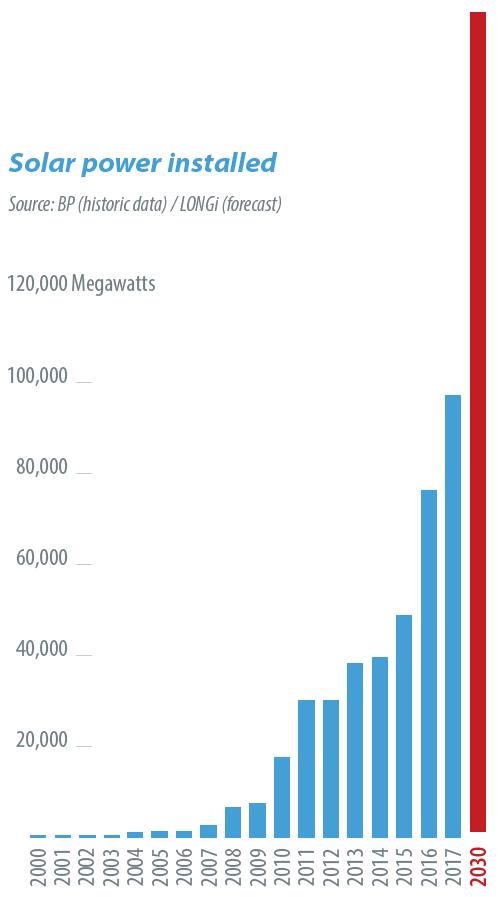

The global solar market has grown at a compound annual growth rate (CAGR) of 24% between 2010 and 2017. There is an undeniably leading role for solar PV as one of the central pillars of the global energy system of the future. Decentralized PV generating capacity is quickly becoming an integral feature of our built environment and mobility infrastructure.

To fulfill expected end market demand for PV modules and products, and for countries to meet their climate-protection goals, global solar manufacturing capacity will have to be vastly increased from the approximate 120 GW in place today. The need for low cost, high throughput, high yield, and energy efficient PV production technologies, in particular CIGS, is becoming increasingly urgent.

Thin film PV, and CIGS in particular, offers one of the most efficient semiconductor materials for the conversion of sunlight into electricity. Thin films require around one hundredth of the semiconductor material when compared to crystalline silicon (c-Si) – including polysilicon losses through mechanical sawing of silicon wafers: 2 micrometers (μm) of semiconductor material compared to 180 μm. CIGS PV’s material usage is thus low, presenting an inherent advantage to it and other thin film technologies.

Thin film PV exhibits an energy payback time of less than 12 months in most parts of the world, and six months in the Sun Belt region. This is a significant improvement on c-Si, which achieves an energy payback time of between 12 and 18 months.

In terms of carbon footprint, thin film PV has a very clear advantage over c-Si. While commoditized mono c-Si has a carbon footprint of 50–60 g CO2 equivalent/kilowatt hour of electricity, the carbon footprint of thin film PV is only 12–20 g CO2 equivalent/kilowatt hour.

This approaches the carbon footprint currently achieved by wind power of 10–12 g CO2 equivalent/kilowatt hour – a significant milestone, particularly given the wide range of applications for which solar PV is suitable.

Recycling and end-of-life issues are becoming increasingly important as the global PV industry continues to scale. CIGS recycling processes are low impact and high value. The European Union, through its member states, is currently leading the way in providing a legislative and regulatory framework to close the loop in terms of PV module lifecycle management. Following a pattern established in other industries, it is likely that other jurisdictions will follow suit in the coming years. CIGS is ideally positioned to fulfill these end-of-life standards.